An offer by Advanced Trials Insurance (Atrialis GmbH)

Clinical trial insurance

On this page, we address all relevant issues relating to the protection of subjects in your (global) clinical trial.

Properly safeguarding of clinical trials

Conducting studies, tests and clinical trials is an important part of many industries, particularly in the field of research and development. It is essential that the participants in these studies are adequately insured. Clinical trial insurance plays a key role here by offering protection to participants while minimizing the risks for companies.

We would like to give you a comprehensive overview of clinical trial insurance: from the basics and legal aspects to the different types of insurance and their importance for your company. Our aim is to provide you with the knowledge you need to make informed decisions and carry out your projects safely and successfully. We will answer the important questions.

Short disclaimer:

Companies from the fields of biotechnology, medical technology and pharmaceuticals are referred to here simply as “life sciences companies” so that the list is not always exhaustive.

The most important questions about clinical trial insurance

What is clinical trial insurance?

Clinical trial insurance protects participants in clinical trials against damage to health that may occur in connection with the trial. This applies in particular to cases in which a person is killed, physically injured or their health is impaired in any way.

The special feature of this insurance is that it is also liable to pay benefits if no one else can be held responsible for the damage.

The cover typically includes:

- Permanent disability: clinical trial insurance provides financial compensation if trial participants are permanently unable to work as a result of participating in the study.

- Death: In the worst-case scenario, the insurance provides financial compensation to the surviving dependents.

In addition, clinical trial insurance often also covers temporary damage to health, depending on the contractually agreed conditions.

The legal basis for this insurance is § 40a of the German Medicinal Products Act (AMG). In addition, Article 10 of the Medical Device Regulation (MDR) prescribes corresponding protective measures for studies with medical devices. Taking out this insurance is not only a legal requirement, but also an important part of the ethical responsibility towards the study participants.

In which cases must clinical trial insurance be taken out?

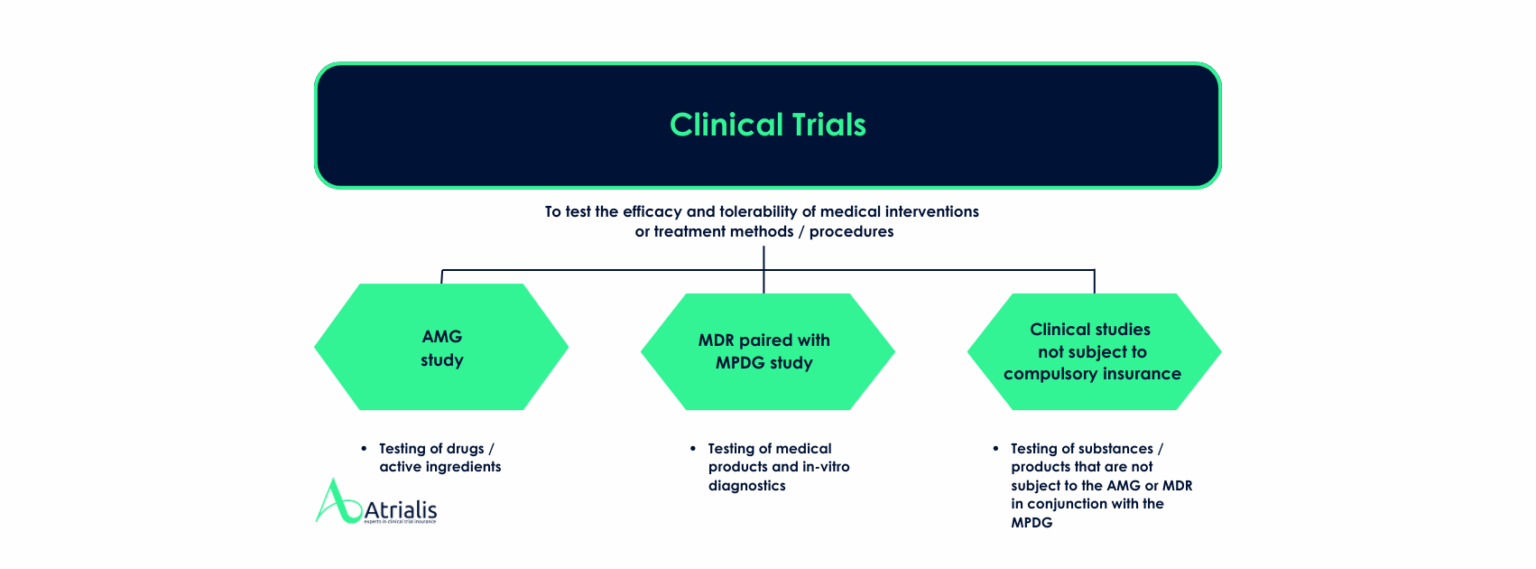

Clinical trial insurance is mandatory in certain cases, in particular for clinical trials for the testing of:

- Medicinal products that have not yet been approved: in accordance with the provisions of the German Medicinal Products Act (AMG).

- New or further developed medical devices: in accordance with the provisions of the Medical Devices Implementation Act (MPDG) and the Medical Device Regulation (MDR).

The conclusion of clinical trial insurance is mandatory and applies regardless of whether there is contractual or tortious liability on the part of the study operator. This means that insurance cover is guaranteed even if no one can be held responsible for any damage that has occurred.

The insurance is taken out in favor of the trial subjects with a specialized insurer that is approved for the scope of application of the AMG or the MPDG. In practice, this is often done through specialist insurance brokers such as us, Atrialis, who specialize in insurance for clinical trials.

Ethics committees also require proof of insurance before they approve the conduct of the study.

Who needs clinical trial insurance?

Clinical trial insurance is mandatory for various players in healthcare and clinical research:

- Pharmaceutical companies and manufacturers of medical devices:

If new drugs or medical devices are tested as part of clinical trials, it is legally mandatory to take out clinical trial insurance. - Clients of clinical trials (sponsors):

Universities, research institutions or hospitals that conduct clinical trials require volunteer insurance to cover damage to participants. - Contract research organizations (CROs – Contract Research Organizations):

When CROs plan and conduct clinical trials on behalf of a sponsor, they must ensure that the necessary insurance is in place. - Study centers and physicians:

Study directors and investigators in clinics or medical practices should also check whether clinical trial insurance is in place before starting a study.

What does clinical trial insurance cost?

The costs for clinical trial insurance vary and cannot be set at a flat rate, but generally range between €30 and €400 per subject. Subjects who are only intended for screening and participants in the placebo group are usually included without additional premiums.

Insurers assess the risk based on the following criteria:

- Investigational drug or procedure: What are the risks associated with the drug or procedure being studied?

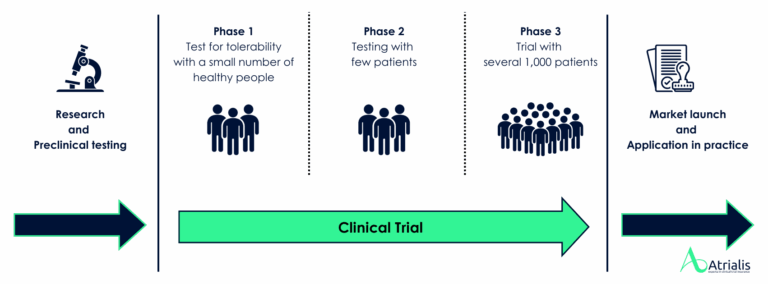

- Study phase: Phase I to IV, CE approval or studies without compulsory insurance.

- Number of participants: The number of test subjects or patients influences the premium amount.

- Countries of recruitment: Recruitment in certain countries may entail additional requirements.

The last point in particular can be decisive, especially if high sums insured are required, such as those demanded by German ethics committees for high-risk studies. National insurers often reach their limits here, despite the additional capacities of reinsurers. This problem often arises with multinational clinical trials. We therefore discuss the optimal insurance solutions with you at an early stage, based on our analysis of the study project.

An insufficient sum insured can be particularly problematic towards the end of the trial. In order to avoid costly emergency solutions, we structure the insurance cover carefully right from the start, for example by working with several insurers. (Keywords: co-insurance and excess liability clinical trial insurance).

When does the insurance cover begin and end?

The insured period begins with the screening phase, i.e. the initial examination by the doctor, but at the latest with the written consent of the test person to participate in the study. A purely verbal question by the doctor (e.g. “Would you be interested …?”) without a physical examination does not count as screening. During the period between the first and last examination, the subject is insured against almost all risks that may arise during the clinical trial. Specifically, this means that treatment errors that occur during an already planned operation are also covered by the insurance. This point is often overlooked.

The study ends for the test person with the final examination. However, the insurer in Germany takes a longer period into account: it covers damage to health that occurs up to five years after the end of treatment, provided that this damage is reported no later than ten years after the end of the clinical trial. This means that the sum insured must be provided over a considerably long period of time.

The following documents are required for new applications for a clinical trial:

- Study protocol (Protocol)

- Patient information / Informed Consent Form (ICF)

- Number of subjects per country (usually under “Number of Patients” in the protocol)

- Questionnaire

- Information on the duration of the study

When is it not absolutely necessary to take out clinical trial insurance?

Taking out clinical trial insurance is not required by law in all cases. In particular, studies that do not test drugs or medical devices do not require insurance.

Examples here are:

- Scientific studies on dietary supplements: Since dietary supplements are not considered medicinal products and do not have a medical curative purpose, they do not fall under the AMG or the MPDG. Studies in this area are often carried out for marketing or efficacy reasons without a mandatory regulatory framework.

- Observational and questionnaire studies: Studies in which only the behavior or habits of test subjects are examined without interfering with their health also do not require statutory clinical trial insurance.

- Non-invasive medical studies: For studies that do not involve any physical interventions or risks (such as pure imaging or routine diagnostics without new techniques), there is no legal obligation to take out clinical trial insurance.

Nevertheless, in many cases it can make sense to voluntarily take out clinical trial insurance for these studies as well in order to provide comprehensive protection for trial participants and create a basis of trust for participation.

Why is voluntary insurance becoming increasingly important?

Even in clinical trials for which there is no statutory insurance obligation, many sponsors take out appropriate insurance to protect the test subjects. We are also increasingly observing that such a promise of cover can be advantageous when recruiting test subjects.

Why we recommend voluntary insurance:

- It serves to protect the volunteer from potential harm.

- It strengthens the trust of potential participants and facilitates recruitment.

- Supplementary insurance, such as travel accident insurance for the journey to and from the study center, is increasingly being offered as standard as additional protection.

Which additional cover is recommended`?

The following additional cover options are often required:

- Travel accident insurance for participants traveling to or from the study site (usually a hospital or research facility or study center). The obligation to the study sponsor for extended care is covered by this insurance.

- Radiation liability insurance: In order to obtain approval (proof of nuclear coverage) from the Federal Office for Radiation Protection (BfS), in some cases the inclusion of radiation liability insurance or supplementary radiation liability insurance is required. These studies use radioactive substances or ionizing radiation for medical research purposes on humans.

What are the special features of insurance for international clinical trials?

International studies require special insurance policies that comply with the respective national laws and regulations. This includes ensuring that the required sums insured are complied with and that the policies are issued in the respective national language. This makes country-specific insurance policies necessary, which must take into account different legal framework conditions, such as varying amounts of cover per subject and specific statutory subsequent liability periods. It must also be ensured that all participants understand the insurance policy in their local language, which is guaranteed by local policies.

Another key point is the provision of no-fault indemnity to ensure the necessary insurance cover in accordance with national requirements. In many countries where your study may be conducted, such no-fault cover is required by law.

It is worth noting how widely the maximum compensation amounts per subject can vary within the EU. There is therefore an increasing trend towards umbrella cover, particularly for multinational studies, in order to ensure that insurance cover is standardized, transparent and risk-appropriate. The statutory upper limits can vary between EUR 29,000 and EUR 5,000,000 per subject, depending on the country. In this case, umbrella cover offers comprehensive protection if the local minimum requirements for clinical trial insurance have been exhausted.

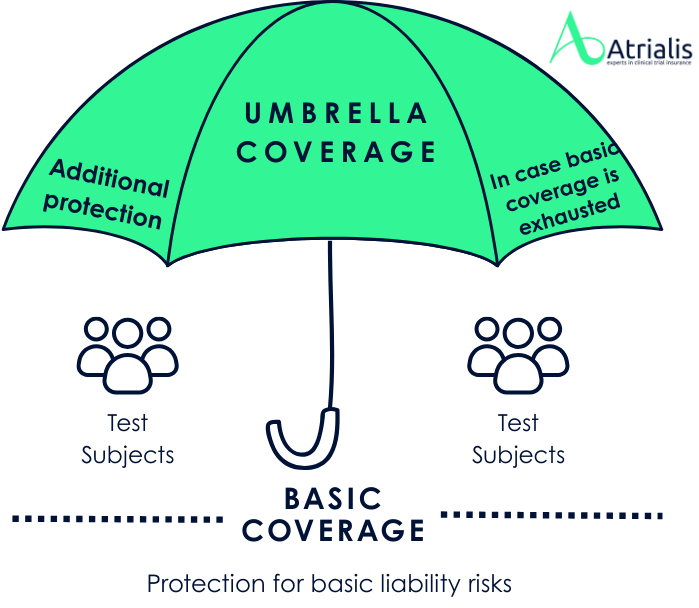

What is Umbrella coverage?

In some countries, particularly the USA, we are observing a trend for trial sites to demand higher amounts of cover for clinical trial insurance than the legal or ethical minimum requirements. While a limit of USD 5 million is considered sufficient by law in the USA, some trial sites require cover of at least USD 10 million per claim and in the aggregate. These additional requirements provide extended protection against potential liability claims that may exceed the statutory limits, as there is no legal limit on liability. One solution may be to voluntarily select a higher sum insured for certain countries or study centers in order to meet their requirements and facilitate recruitment efforts.

This is where umbrella coverage comes into play, which provides additional protection like a protective umbrella when the basic clinical trial insurance cover has been exhausted. Such cover can also be useful if, for example, an extended reporting period (ERP) is required by extending the insurance cover for the desired or required duration. Usually, umbrella cover is underwritten by a different insurer than the original clinical trial insurance, which allows for better and more flexible negotiation of cover amounts, premiums and cover contents (such as the ERP term). Weaknesses in the basic insurance can thus be compensated for by the umbrella solution.

Advantages of umbrella coverage for the sponsor of the study:

- Increased attractiveness in the recruitment of study centers and subjects/patients due to the improved, voluntary insurance cover.

- Emphasis on the sponsor’s duty of care by offering more than the legal minimum, which is also positively received by ethics committees.

- Additional protection against liability cases that go beyond the legal requirements, and thus also better protection of the sponsor’s own reputation

- Uniform and risk-adequate protection for multinational studies, with clear transparency and consistency in the cover.

Why Atrialis is your suitable partner for clinical trial insurance

We are an independent and specialized insurance broker for life sciences companies and have a particular focus on insurance concepts for liability risks of managing directors. With our experienced team of lawyers, risk managers, business economists and insurance brokers, we see ourselves as a partner for game changers in all matters relating to risks and liability and can keep pace with the dynamic growth of your life sciences company with suitable risk and insurance solutions – we are happy to help with our trial subject cover for clinical trials.

However, we also advise well-known life sciences companies on capital market liability issues and support biotechs with special insurance solutions, for example in the context of financing rounds and IPOs (e.g. on the NASDAQ). We are happy to contribute the experience we have gained from assisting with the insurance issues of some of the most prominent US IPOs of German biotech companies in recent years.

Specialized

We are one of the leading insurance brokers for the coverage of clinical trials!

Worldwide coverage

In addition to excellent access to London, we are experienced in securing worldwide studies.

High Service Level

Only a few hours left until the ethics committee meeting and no insurance? Give us a call!

Do you need assistance?

Please call us directly or enter your preferred date for a callback or video conference:

Your Atrialis Team of Experts:

Florian Eckstein

Managing Partner

Björn Stressenreuter

Managing Partner

Jutta Zaglauer

Life Sciences Expert

Dr. med. Thomas Lacina

Medical professional

Dr. rer. biol. hum. Manuel Kistler

Expert for medical technology / products

Franziska Fink

Financial Lines Expert

Miriam Born

Lawyer